SPAN Parameter Files

DCCC implements the Standard Portfolio Analysis of Risk (SPAN) based Risk Management System using the SPAN framework licensed by Chicago Mercantile Exchange (CME). SPAN is a globally accepted portfolio based approach that determines portfolio margining requirements for futures, options, cash, and other instruments.

SPAN considers 16 “what if” scenarios where futures prices and volatilities are altered to varying degrees. The largest loss (represented by a positive value) across the 16 scenarios becomes the SPAN margin for that portfolio.

There are 4 Intraday SPAN runs at 6am, 10am, 3.00pm and 6pm, as well as an End of Day SPAN file at 11.55pm. All 5 files can be found on the Members FTP. In times of high volatility, DCCC may generate additional SPAN files, dependant on perceived risk. An announcement will be made to members before these additional files are generated to ensure their obligations can be met.

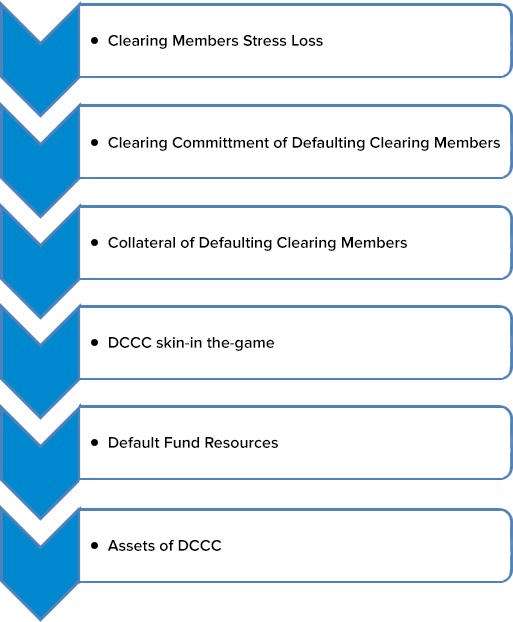

Default Management

DCCC has implemented a Default Fund (DF) that is sufficient to cover the losses of the two-largest Clearing Members (Cover-2). DCCC’s own contribution (“skin-in-the-game”) is approximately 35% of the total DF.

In the event of a default of a Clearing Member losses incurred in the management of the default would be met using the following Default Waterfall.

Credit Interest on Default Fund Contributions

DCCC shall pay Clearing Member’s credit interest on their Default fund contributions at a rate of 1.89% per annum for contributions from July to September 2024.